Your Quarterly HR Tech Funding Update

The first quarter of 2023 presented a complex landscape for funding rounds. Inflation remained stubborn, central bank continue to rise interest rates, and we witnessed the sudden collapse of the Silicon Valley Bank (SVB) which influenced the market dynamics for startups. Despite these challenges, the HR Tech sector demonstrated resilience and adaptability.

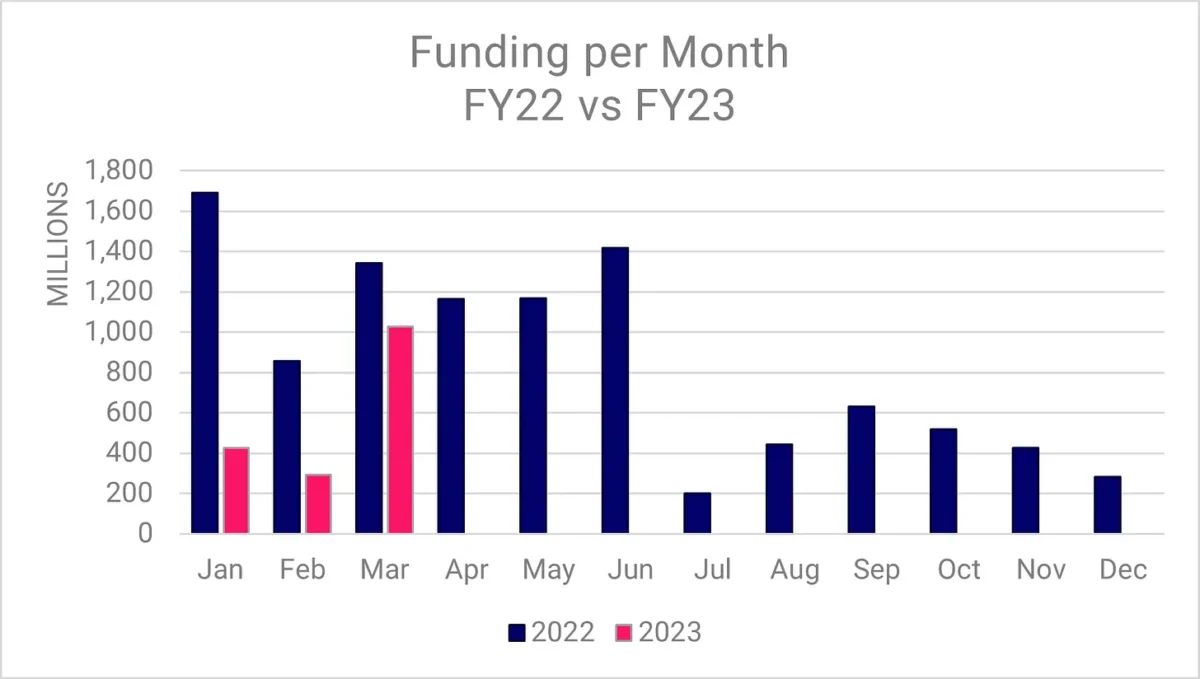

When we look at the year-on-year indicators, Q1 2023 paints a concerning picture: the number of funding rounds dropped by 39%, total investment plummeted by 55%, and average deal size declined by 27%. But keep in mind that the fallout of the war in Ukraine did not show until after the first quarter of 2023. Before that date, the funding market was booming. Although year-on-year indicators show a downturn, comparisons with Q4 2022 suggest a more optimistic outlook.

Q1 2023 saw HR Tech investments surpass $1.7B, a 42% increase from Q4 2022 ($1.2B). Note that when we exclude Rippling’s substantial $500M Series E emergency round after the fall of SVB, the quarters are mostly equal. However, 6 companies did not disclose the funding amount. Series A rounds were particularly active, growing by 31% compared to the last quarter, while Series B rounds remained stable. Seed rounds also increased by 20%. Later-stage VC investments were mainly driven by Rippling’s $500M emergency Series E financing.

HR Tech takes a financial turn

In a rapidly evolving market, HR Tech vendors are adapting to capitalize on new opportunities. In my 2022 annual review, I shared my observation that investors were funding more startups that are focused on the optimizing the financial aspects of employee relationships. This trend persists, with HCM & Pay, Financial Wellness, and Benefits leading in terms of deal value.

HCM & Pay refers to comprehensive HR suites that may or may not include a payroll engine. Financial Wellness is a category that includes tools and platforms that help employees manage their personal finances, while Benefits encompass solutions designed to streamline the administration of employee perks and benefits.

Talent Acquisition and Talent Management follow in place four and five. However, excluding Rippling’s massive round, HCM & Pay falls to third place. It’s the first time in over two years that this category doesn’t outperform the others by far.

With $38M in funding, compensation isn’t the largest category, but it’s the fastest growing one. This surge started last year, and the new Equal Pay legislation will certainly ensure this remains a growing category.

Also interesting is that funding for solutions to pay the Global Workforce fell considerably: While in the first three quarters of 2022 the category attracted hundreds of millions per quarter, in Q4 the category attracted $23M while in Q1 only 2 companies received seed rounds totaling $2M. Which makes me wonder if we have seen peak performance? I mentioned in an earlier article that these companies often sell their services to so-called “high-growth” companies and wondered how the ongoing tech layoffs would affect them, considering these are all high-growth companies…

Analytics performed really well, doubling year on year in value from $10M to $22M and keeping track with last quarter. Companies continue to be interested in understanding how analytics can contributed to increased productivity. The interest in Mental Health solutions continues their declining trend: from $79M in Q4 to $7.6M this quarter.

Integrated payroll is back!

One notable shift I see is an increasing number of HCM Suites that come to market with an integrated local payroll engine. For a long time, founders created HCM suites that were focused on servicing the global workforce with an integration to a 3rd party payroll. New solutions adopt a more regional approach, launching in one country and then expanding to neighboring markets. This trend is particularly interesting, as it signifies a departure from last year’s more global focus. I believe this shift reflects an industry-wide recognition of the need (and opportunity) to customize HR Tech solutions to cater to diverse regional regulations and cultural nuances.

When you launch a local solution, you must include an integrated payroll, especially when it is aimed at the SMB market. It’s expected and it makes your product sticky. Switching payrolls is much harder than replacing one HCM solution with another. I also saw several solutions that focus on serving a specific part of the market, like facility or health services. This strategic shift highlights a growing demand for industry tailored or region-specific solutions, that are better in catering to specific, local workforce needs, providing HR Tech vendors with new avenues for growth.

Funding: A Regional Landscape

I counted 90 funding rounds in the first quarter of 2023. American companies receive most of the HR Tech funding, accounting for 45% of deals. The total number of funded countries fell to 24, a significant decrease from 46 countries in Q4 202. Europe came in second with 27% of funding rounds.

Latin America’s HR Tech funding hit a low point in Q4 2022 with only one funding round. Q1 2023 wasn’t much better with only three Series A and B rounds. I could not find any seed rounds for Latin America, and that is concerning: it suggests a lack of early-stage investment activity. Seed funding plays a crucial role in nurturing innovation and fostering a robust pipeline of future HR Tech solutions.

Asia experienced a 57% year-on-year decline in total venture funding, even though the number of deals increased from 8 in Q4 2022 to 11 in Q1 2023. We should keep a close eye on Asia’s HR Tech landscape, as the region’s diverse markets and large talent pool are likely to foster innovative solutions in the long run.

A few weeks ago, I wrote about the promise of the African startup ecosystem. African HR Tech vendors maintained a steady presence and secured four deals in Q1, consistent with Q4 2022 figures. The region’s large, organic market opportunity presents a compelling case for investment in HR Tech startups. African startups have the potential to create tailored solutions that cater to the region’s unique needs and challenges, ultimately enhancing the lives of millions of workers and organizations across the continent. I am eager to see how African HR Tech vendors will capitalize on this potential and contribute to the global HR Tech ecosystem.

The AI Revolution: Harnessing ChatGPT

The introduction of ChatGPT 3.5 and 4 has sent shockwaves through the tech world. Many HR Tech vendors are racing to announce in press releases that they have integrated this powerful technology into their solutions, touting its potential to revolutionize employee engagement, recruitment, and performance management. Even though the technology has only been publicly available for three months.

As with any emerging technology, I suggest approaching ChatGPT integration with caution. While ChatGPT’s potential is immense, it’s essential to thoroughly evaluate its real-world impact on your HR processes. We have seen too many examples where ChatGPT didn’t get it quite right. And when answering employee questions, that is not good enough: you must be exactly right. I’d recommend to learn, experiment and proceed with caution. When you make integrated AI services available in employee services, ensure that you know exactly what it does under the hood. Just for the off chance you might need to explain it to a judge…

Resilience and innovation in uncertain times

When I wrote my 2022 annual analysis in January, I concluded that we had returned to a focus on fundamentals and that was long overdue. It’s clear that the fast and massive rounds are over. Investors are more careful and scrutinize the pitch decks in much more detail than before. In line with that observation, the first quarter of 2023 brought a mixed bag of results for the HR Tech industry. While some indicators, such as seed round activity and a growing number of deals compared to the prior quarter suggest a positive trajectory, other factors, like the decline in the number of countries with deals and a cautious approach to late-stage investment, paint a more uncertain picture.

The “participate at all costs in a hot sector” stress of 2022 has gone away. Investors are more selective and only back the best startups or none at all. At the same time, I continue to see new names join the list of VCs that invest in HR Tech startups, as well as an increasing number of angel investors (stemming from more seed rounds).

Despite the uncertainties, there are enough reasons to remain optimistic about the future of HR Tech. The growth in early-stage investment activity demonstrates that venture capital firms are willing to support the next generation of innovative startups. The ongoing interest with a focus on financial aspects of employee relationships, in areas such as financial wellness, benefits, and HCM & Pay indicates a continued focus on creating holistic, employee-centric solutions. The continued stream of young HR Tech solutions to meet evolving market demands, regional expansion strategies, and a focus on financial aspects of employee relationships all signal exciting prospects for the industry’s future.

The rapid development and integration of AI technologies, such as ChatGPT, offer exciting opportunities for HR Tech vendors. However, it’s crucial for companies to experiment cautiously and prioritize long-term value creation over short-term hype.

At the same time, I find it concerning that we didn’t see any more funding going to later stage, more mature, companies. The fact that regional (non-US focused) investments are down does not indicate that the worst is behind us.

Did we see the floor in VC investment in the last quarter? No one really knows, but the first quarter of 2023 was a solid quarter for VC investment in HR Tech and as usual, I will keep you posted of what happens in the next quarters. Let’s see who can adapt to and seize the opportunities in this dynamic environment.