The Future of HR Tech: Key Insights from 2023 Investments

I start to prepare the annual report at the end of the year. I double check the numbers, see if I’ve missed anything and by January 1st, I’m ready to write the overview. When I start the analysis, I always find more interesting angles to look at. What if I slice the data in a slightly different way? What if I look at it from a regional perspective? Did I miss any trends worth mentioning? In other words, once I start dissecting the data and create the charts, it’s hard to stop. But I must, because otherwise this article wouldn’t appear until February, and it would be so long that you won’t read it. So, let’s make a deal: in this article, I focus on the highlights: services, funding stages and geographies. And if you have a question that I didn’t discuss, please let me know and I’ll see if I can answer it. Deal?

Exploring 2023’s HR Tech Investments

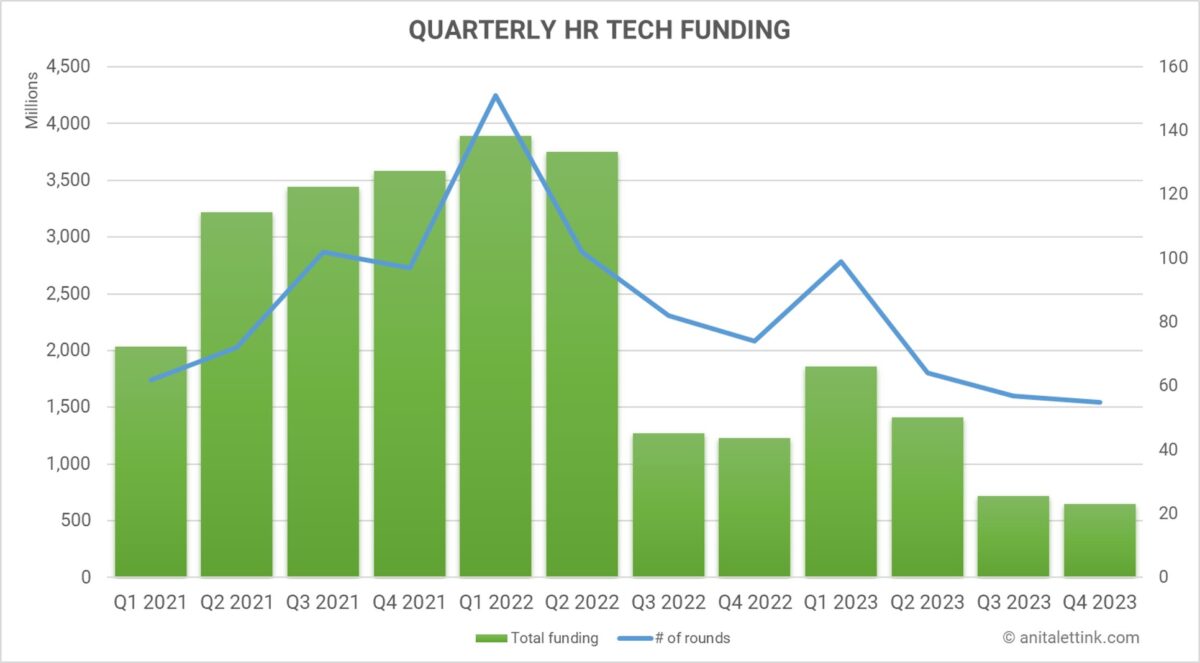

The HR Tech sector in 2023 faced a challenging investment landscape that was characterized by economic uncertainties (persistent inflation and rising interest rates), fluctuating markets, and shifting funding trends. And that was reflected in the funding rounds: unfortunately, we continued the downwards trajectory from the peak in the second quarter of last year.

The final two quarters of 2023 were particularly weak in comparison to prior years. Investors pared back spending at all stages. The only favorable exception was seed stage rounds, which held its own and continued to flourish.

The total amount raised was $4.6B over 275 rounds in 38 countries. That’s a 33% decline in rounds compared to last year and a 55% decline in funds raised. The chart shows the overview of deal count and value for the last 12 quarters:

Here’s a short summary of the highlights if you don’t have time to read the full article:

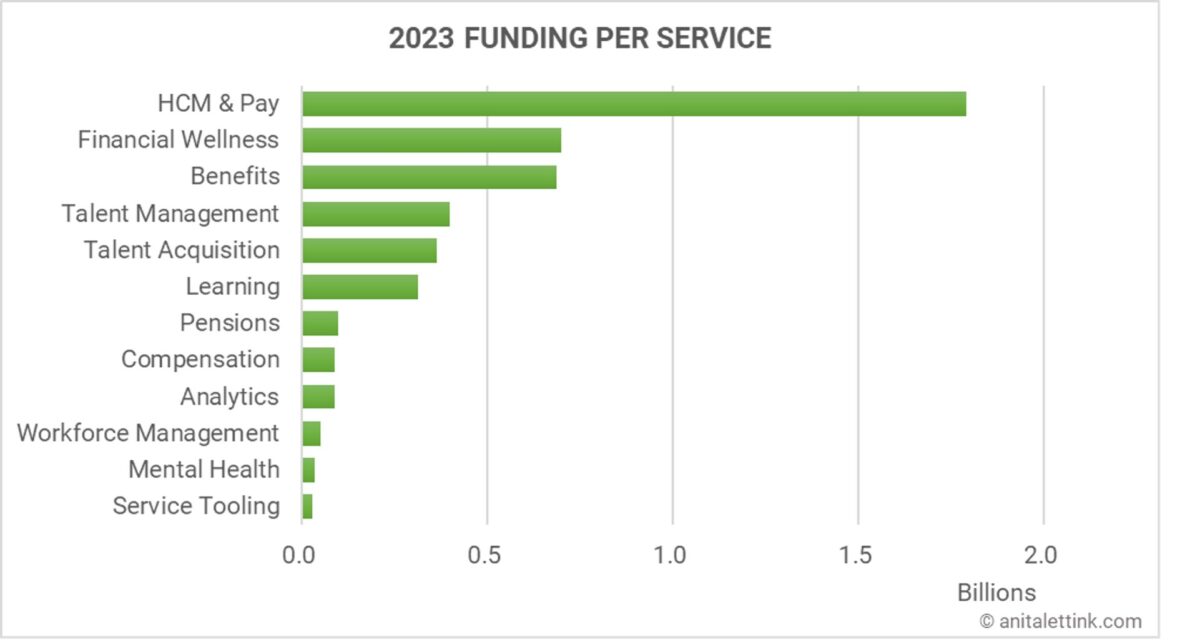

- HCM & Pay remains the largest category at $1.8B

- Local HCM Suites incl payroll are popular

- Global Workforce solutions & multi-country payroll are down significantly

- 70% of investments go towards administrative and financial HR services

- HCM Suites

- Payroll

- Benefits

- Compensation

- Financial Wellness (esp. earned wage access

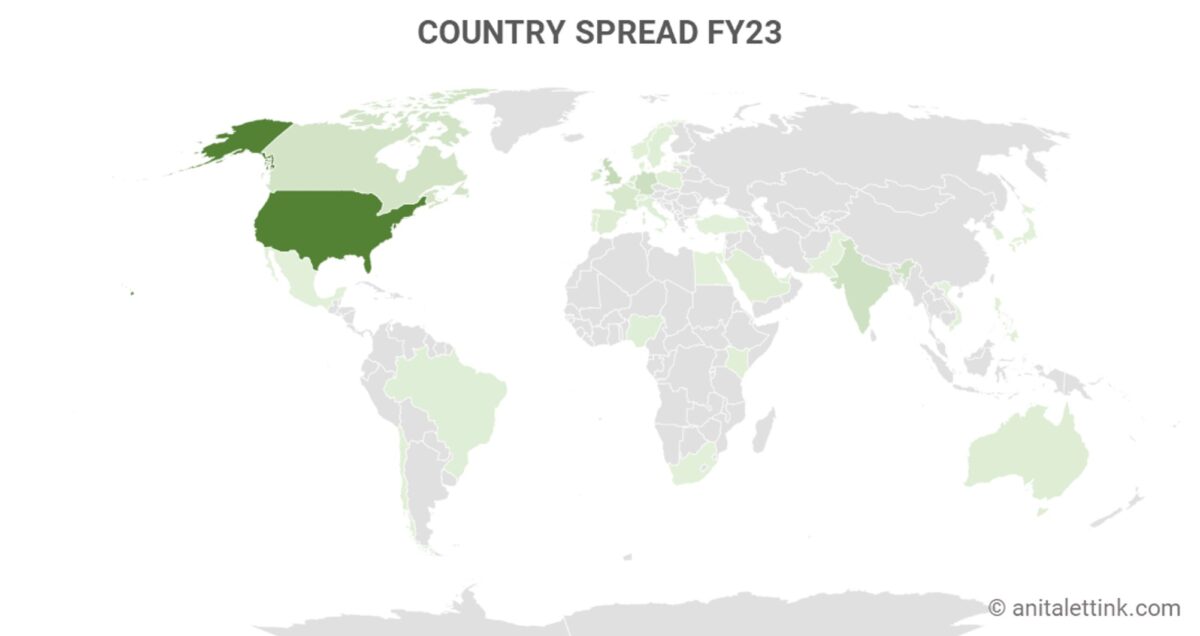

- HR Tech Funding is going local: 61% of rounds are outside US

- 52% of rounds are seed or earlier

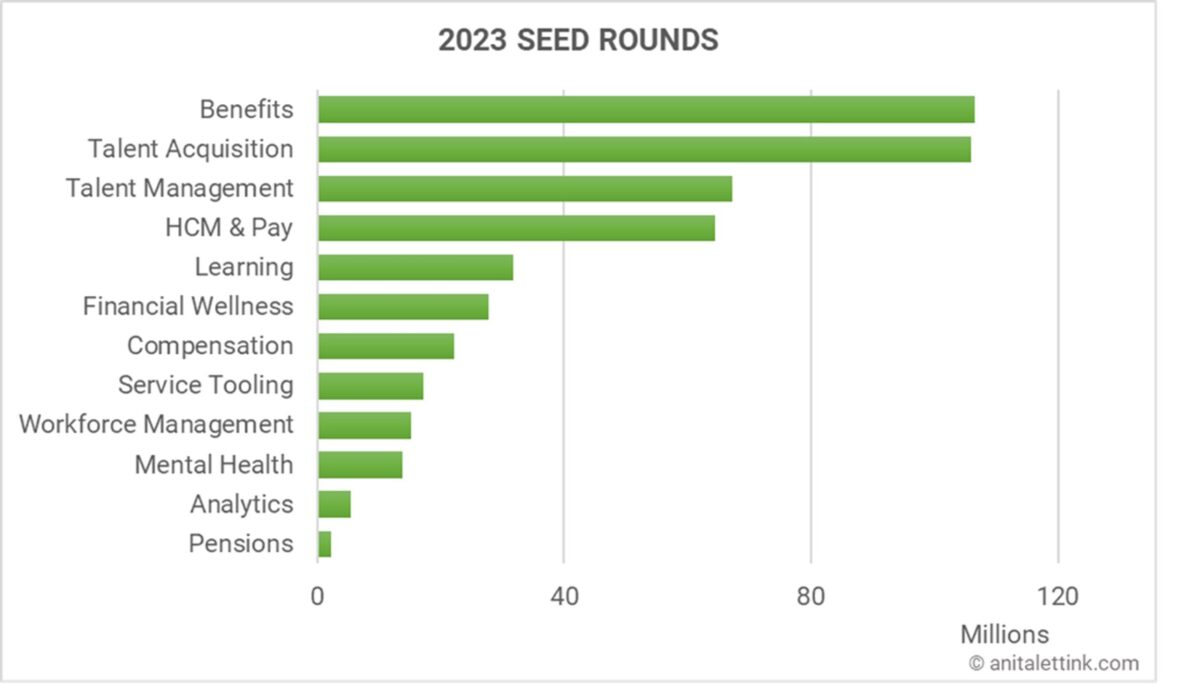

- Benefits is the largest in funding ($107M)

- Talent Acquisition is largest in # of rounds (37), AI-based solutions dominate

- Average investment is $17.9M

- More angel investors involved than in prior years

- Unlike prior years, few investors were involved in two or more rounds. The sector could use more focused investors that can support founders with in-depth knowledge of the HR Tech market.

The Role of services in 2023’s HR Tech

As in prior years, HCM & Pay services dominate the funding landscape with a significant investment of $1.8B over 42 deals, highlighting the market emphasis on administering and paying the workforce through comprehensive human capital management and payroll solutions.

In 2021 and 2022, the growth of this service category was driven by massive investments in solutions to manage and pay the global and remote workforce (esp. EoR services). In 2023, these solutions did not attract any substantial funding– we seem to have reached peak interest and maybe even market saturation, with some of these vendors downsizing and laying off employees. The HCM & Pay category remains the largest because of renewed VC interest in funding local HCM Suites.

I noticed an increasing number of HCM Suites coming to market with an integrated local payroll engine and that’s a great development. For a long time, founders created HCM suites with an integration to a 3rd party payroll. Payroll is one of the hardest solutions to build, but necessary to have. It also makes an HCM Suite more sticky, as migrating payroll is a risky HR project. These new solutions adopt a more regional approach, launching in one country and then expanding to neighboring markets. This is especially important for emerging markets, where these suites are new and can easily achieve double digit market growth.

Financial Wellness and Benefits services attracted nearly $700M and $686M, respectively. In my 2022 annual review, I shared my observation that investors were funding more startups that are focused on the optimizing the financial aspects of the employee relationship. Financial Wellness rounds predominantly contain so-called Earned Wage Access providers, that allow employees to request (a part of) their earnings before pay day. The substantial funding for this category underscores a shift towards holistic employee well-being, emphasizing that today’s workforce needs more than just a paycheck; they seek financial security and a comprehensive benefits package.

Talent Management, Talent Acquisition and Learning continue to attract investments, reflecting the ongoing need for recruitment, development, and learning within HR tech. Almost all Talent Acquisition solutions boasted some sort of generative AI functionality. The focus on individualized talent approaches that started last year continued with an influx of digital employee coaching solutions, that claim to offer personalized approaches in an efficient way. The number of rounds suggests that while the need for effective talent strategies and continuous learning is obvious, the market may be approaching a saturation point, or investors are becoming more selective, and waiting for innovative performers that tackle the thorny issue of re- and upskilling employees.

I found it surprising that Pensions and Compensation received much less funding than in 2022. Considering the rise of Pay Transparency legislation across the globe, most notably in Europe, I expected to see more founders come to market with solutions to support Equal Pay for Equal Work efforts. Companies will not be able to satisfy the requirements of e.g. the EU Pay Transparency Directive by relying on their HCM suites. They need much more focused approaches, supported by solid analytics. On the other hand, this is a very specialized and specific HR service that not many founders may have experience with. With new ways to reward employees being introduced, compensation is underfunded and needs more attention from founders and investors.

Overall, funding rounds for services like Analytics, Workforce Management, Mental Health and Service Tooling are declining. This is caused by a variety of scenarios, but the presence of established players in combination with a limited scope for disruption seems to be the most plausible explanation. I first noticed the trend to fund Financial instead of Mental Health solutions last year, and it has picked up since then. Workforce Management solutions, another one of the more complex services due to local legislation, could use more founders that offer customers options besides the incumbents. And the market for stand-alone HR Analytics seems to slowly give way to integrated dashboards in HCM suites or generic analytics platforms already in use at companies.

How did funding stages hold up?

In 2023, seed, pre-seed and angel rounds were less impacted by the market downturn than early- and late-stage rounds. Both the number of seed rounds and the investments were at a similar level compared to last year: 143 at $481M in 2023 compared to 149 at $482M in 2022. This also means that the average investment hardly moves. The funding pullback was particularly pronounced for early and late-stage rounds, where a lackluster IPO environment dampened dealmaking and round sizes. The number of early and late-stage rounds halved compared to the prior year.

Seed Stage Dominance: With 143 rounds, the ‘seed or earlier’ stage attracted the attention of many investors. This finding suggests a continued and vibrant ecosystem of new startups in the HR technology space, indicative of ongoing innovation and the opportunity for new players to enter the market. Investors continued to fund seed stage companies at the same pace as in prior years. These rounds obviously require lower investment amounts (average is $3.4M) with a potential for higher returns on investment.

Last year, the top 3 funded services were Talent Acquisition, Talent Management, HCM & Pay. In 2023, Benefits just beat Talent Acquisition to the top spot, followed by Talent Management. Benefits startups often deliver specialty services, with a focus on e.g. mobility, bereavement, or reproductive services. And while the average investment in seed rounds is $3.4M, I noticed that Benefits founders attract almost double that amount, at an average of $5.9M per round.

Limited Early and Late-Stage Rounds: As we look at later stages, there is a sharp decrease in the number of rounds. Compared to last year, Series A and B rounds dropped significantly. The pullback in series A was 51% and series B 58%. Even fewer companies reached the later stages of funding (Series C to F), with the numbers ranging in the lower single digits. The data suggests that there are challenges in scaling up, or perhaps investors are still waiting to see which models prove sustainable in the long term.

From an optimistic perspective I could say that an unusually high number of companies were able to secure funding in the prior two years (2021: $12B and 2022: $10B) and by now have contracted enough revenue (ARR) to finance their ongoing operations. But it could also mean that the funding climate simply wasn’t there, and in 2024 more companies will either put themselves up for sale or end their service delivery and shut down. I’ve noticed a high number of M&A activities in the sector, indicating that companies choose an exit to join forces with others. While there are enough companies tracking M&A activities, I will do a deep dive into the current state of recently funded companies in an upcoming article.

What about regional HR Tech investments?

The dominance of the US in funding rounds stands out, but it is also declining year over year, and in 2023, 61% of funding rounds took place outside of the US. The US is a great environment for startups. Many companies that were founded elsewhere move their headquarters there once they are ready to raise funds.

However, the “one size fits the globe” approach, by which I refer to a solution developed in the US and then rolled out across the globe with slight adjustments, is not the best approach for HR Tech. Countries have specific legislations and HR policies that need to be accommodated for at the design stage, not bolted on once a vendor decides to sell into other markets. From that perspective, it’s great to see that despite the lower number of rounds raised, the number of countries where companies raised funds did not decline as much (about 10%). In addition, all regions were represented. Even so, compared to last year, the Latam region pulled back the most. And with one of the largest and youngest populations entering the labor force, this is a region that needs an innovative and vibrant HR Tech market.

A short note on Generative AI

For all the buzz around generative AI, it didn’t factor into more than Talent Acquisition seed rounds. As I emphasize in my keynotes, AI in Talent Acquisition is not new. We’ve been using it for years in applicant tracking and selection systems. Even though many HR Tech vendors announced some sort of gen AI feature in a press release, it wasn’t material to the solutions itself. I did see a few promising seed rounds in other categories towards the end of the year, but it’s too early to say if these solutions offer something profoundly different. This area is on my “watch and discover” list for 2024.

When I put it all together

The HR tech sector has experienced a roller coaster of investment activity over the past three years, with a hot streak of funding and innovation, especially in comprehensive HCM solutions and financial employee benefits programs. However, the significant decrease in funding amounts and rounds in the second half of 2023 indicates that the industry might be facing challenges that come with a more mature investment climate, such as market saturation and economic downturns.

This leads to a more cautious investment approach that continues to reward small, innovative founders with seed rounds. Despite the decrease in late-stage funding rounds, the abundance of early-stage investments suggests that the sector continues to attract new ideas and solutions, albeit with an emphasis on clear value propositions and sustainable business models.

2023 HR Tech Funding in three bullets:

- HR Tech Funding Trends Down: The overall trend in HR Tech investments over the last three years showed an initial surge that peaked in Q1 2022, followed by a steady decline. This suggests a market that is entering a phase of consolidation after a period of significant growth. In 2024, let’s see if Generative AI can innovate how we deliver HR Services and bring some much-needed growth.

- Service-Specific Funding: The distribution of funds across various HR services indicates a strong emphasis on administrative and financial services to support the employer-employee relationship. HCM & Pay (with a focus on solutions for local markets), Financial Wellness, and Benefits were the categories that attracted the most funding.

- Funding Rounds by Stage: The data shows a heavy concentration of investment in seed rounds, with a dramatic drop as companies progress to early and later stages. This implies a market that favors the potential of new entrants and adopts a “wait and see” approach as these startups mature.

If you are an HR leader, the distribution of these investments indicates the industry’s pulse – where to innovate, what services to enhance, and how to align your strategies with market movements. For startup founders, it’s important to note these trends as you identify niches and opportunities for disruption (pay attention to Compensation!). And if you are investing in the HR Tech space, it’s about discovering the subtleties in these funding patterns. The big bets on HR Suites and financial well-being point towards long-term value creation in the employer-employee relationship, while smaller, yet significant, investments in emerging areas suggest potential future trends.

And I’ll end on an optimistic note: The prevalence of seed rounds indicates a steady influx of new founders around the globe, who bring disruption, competition, and diversity to the industry. I hope that despite the tough economic challenges, the HR Tech sector can maintain its resilience and adaptability, and set the stage for renewed growth in 2023!

Scope:

This overview focuses on HR Tech solutions that directly support the HR or People function and are most likely to be procured by CHRO’s and their teams.

That means that the following solutions are excluded:

- Job boards

- Marketplaces for independents

- Course platforms and EdTech (a category by itself)

- Solutions for gig workers

- Virtual office environments

- Event platforms

- WorkTech solutions: digital workplace and productivity platforms